How my first Lululemon purchase turned me into a shareholder

As a recently converted yogi

As I’ve started practising yoga on a more regular basis, I’ve noticed a common trend among yogis.

They all wear Lululemon (the females especially).

Even some male yogis wear the brand.

This made me curious.

“Is Lululemon that great?”

“It’s so expensive and yet so many people can afford it?”

So I headed to the nearest Lululemon store to try out their products.

And boy was I amazed by the entire customer experience.

In most stores, when we walk in, the retail staff will either ignore you or follow you like a hawk (for commissioned salesmen).

There was none of that with Lululemon.

I was given the time and space to slowly browse.

When I picked up a few pieces of clothing to try on, I was led to the changing room by one of the staff, who asked me for my name.

Subsequently, the member of staff started addressing me by my name.

They even hung a tag with my name on it outside the changing room which I occupied.

This may not seem like a big thing, but it makes the whole customer experience more personalised.

It’s unlike any other retail experience I’ve had anywhere.

It ended up shelling out 3 digits for 2 pieces of clothing.

Yes, the sucker in me.

How Lululemon makes money

It’s not hard to tell how Lululemon makes money - by selling athleisure wear at premium prices.

As a customer myself, the clothing is incredibly comfy, the prices not so.

The reviews back this up.

Lululemon used to be a brand associated with women’s sportwear and yoga.

But in recent years, the company is increasingly penetrating into the men’s market.

In fact, it was only in 2004 that Lululemon started selling men’s apparel.

The men’s range brought in US$526.5 million in FY 2017 (20% of total revenue).

This number grew to US$2.3 billion in FY 2023 (23% of total revenue), giving it an annualized growth rate of 27.4%.

In 2022, Lululemon announced they call a Power of Three X 2 growth plan.

This is a 5 year plan where the company aims to double their revenue of $6.25 billion to $12.5 billion by 2026.

The plan focuses on three key growth drivers - product innovation, guest experience and market expansion.

The growth drivers underpinning the company’s 5-year plan would likely come from 2 areas:

International sales (China mainland and rest of the world)

Men’s product revenue

These are the segments forming a smaller part of the company’s revenue, the ones which are growing at the fastest clip.

Does Lululemon have a moat?

There’s no doubt that Lululemon operates in a competitive and fast-changing industry.

When it comes to fashion, consumer preferences can change in an instant.

While the company is doing well now, we need to observe how they continue to innovate and invest in its brand.

Its moat can be summed up below.

Direct to consumer model

Lululemon operates on a direct-to-consumer model. This means that they don’t use intermediaries when selling their apparel.

Unlike their competitors, you will not find Lululemon products in third-party retailers like Foot Locker.

This allows the company to retain its brand image and command premium pricing.

Strong Brand

Brands with a cult-like following tend to do well.

Think Apple and the long queues every September when the new iPhone is released.

Similarly, Lululemon seems to have achieved this in the athleisure space, which is no easy feat.

High quality premium products

The materials used in Lululemon’s apparel set it apart from competitors.

The company’s commitment to durability ensures that Lululemon garments outlast those of other brands, reinforcing the brand’s value proposition and customer loyalty.

As a customer myself, I can attest to this (although I might be biased).

Risks

With all that said, there are some risks that we should be aware of.

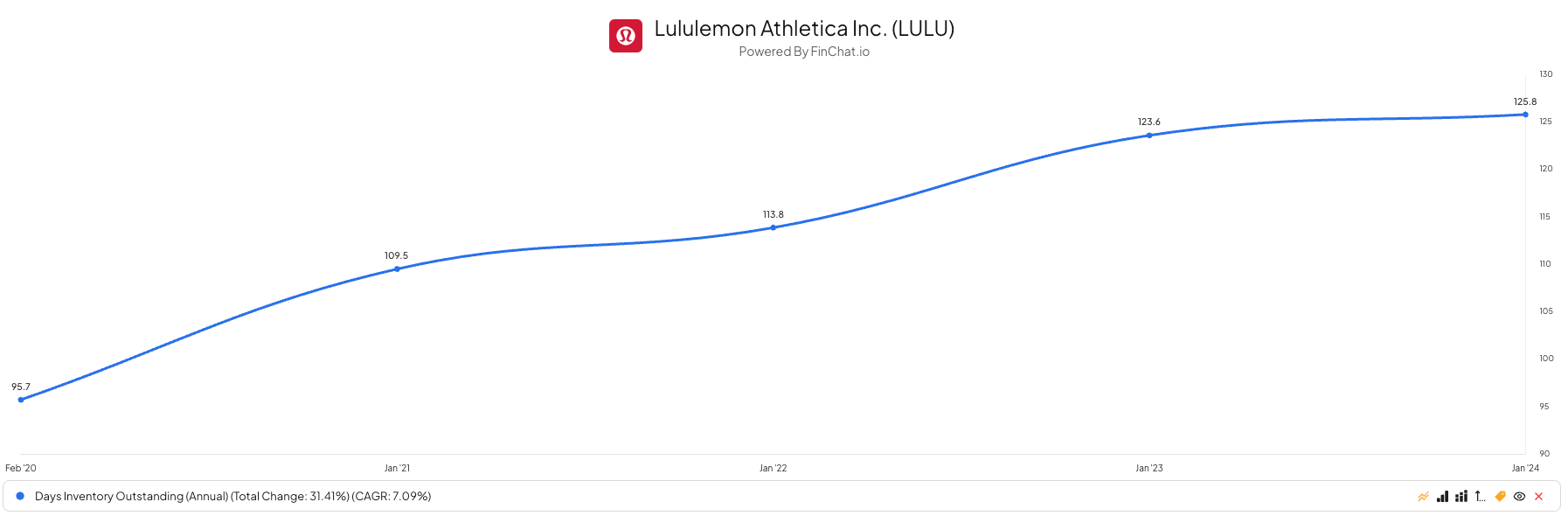

Days inventory outstanding

Days inventory outstanding (DIO) measures the average number of days that a company holds inventory for before turning it into sales.

This metric has been on the rise in the last 5 years.

It suggests that the company may be holding too much stock, and are not selling its products fast enough.

As of now, this is not a huge concern but one to monitor over the coming years.

Failed acquisitions

The company has only had one acquisition so far - Mirror, a fitness platform, blowing $500 million in the process.

Even though this may have been a failed acquisition, it shows that the company is actively working on improving their product offerings, something which I admire.

Given the ample amount of cash that Lululemon has on its balance sheet, this sum did not have a significant impact on the company’s bottom line.

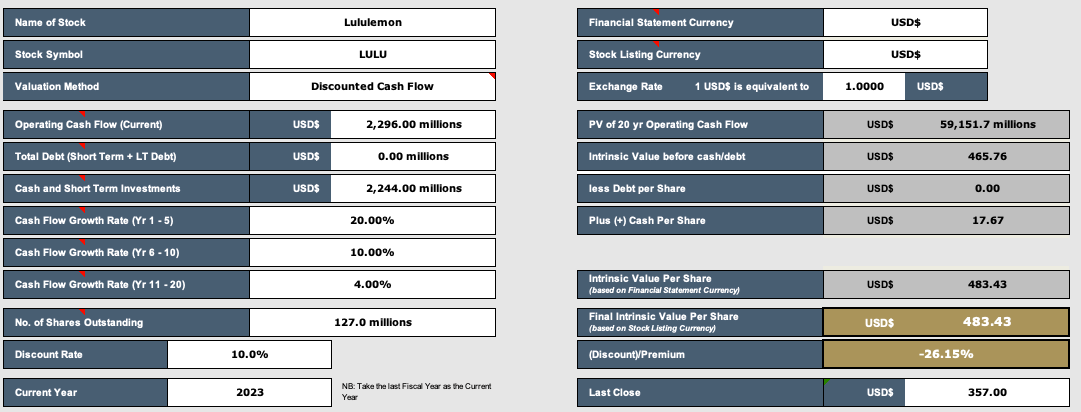

Valuation

The final piece of the puzzle is the valuation.

For an already profitable company like Lululemon, using a DCF model is the simplest way to value the business.

The biggest variable in a valuation model is the growth rate and discount rate. Depending on what rate we choose, the intrinsic value will be different.

It’s why 2 people can come up with different values even when using the same model.

Personally, I like to have a margin of safety by buying at least 20% below my intrinsic value.

This way, even if my assumptions are wrong, I have a buffer that protects my downside.

“Price is what you pay. Value is what you get.” -Warren Buffett

I hope you enjoyed reading this piece as much as I did writing it.

If you’d like to connect, I am spending a lot more time on Twitter/X these days. Follow me over there for more investing and personal finance content