Disrupting the Giant: Is Adobe's Reign Ending?

Analysing Adobe's Strengths and Vulnerabilities in a Rapidly Evolving Market

Adobe is a company who should be no stranger to us, especially if you’re in the creative industry.

This is a company that has been on my watchlist for years.

The only reason why I haven’t bought into it - the stock always seems to be over-valued.

Now that valuations have come down to an attractive level, it’s time to take a closer look.

When a stock keeps going down despite the company reporting good earnings, it’s normal to doubt whether it’s the market or investors that’s getting it wrong.

If you subscribe to the efficient market hypothesis, then the stock market is rarely wrong.

But is it really?

A good example is Meta. The stock was down 70% off highs in 2022 due to the failure of its much-hyped metaverse. Many believed the company was doomed.

Investors over-looked the fact that the metaverse only forms a tiny portion of the company’s business.

Coupled with its low debt and huge cash position, Meta was never going to die in the near-future.

It was a no-brainer to scoop up some shares at those depressed prices.

So, the market may not be so efficient after all.

While it’s not a like-for-like situation, we’re seeing a similar thing with Adobe.

For 2 quarters in a row, Adobe’s stock dropped significantly after reporting (good) earnings.

The company’s stock price is now in a 40%+ drawdown, its second largest drawdown in the last 5 years.

The market believes that Adobe’s fundamentals have deteriorated.

Based on its recent earnings reports, this doesn’t appear to be the case.

How Adobe makes money?

Digital Media (72.5%):

This segment is a major revenue driver, encompassing the Creative Cloud (Photoshop, Illustrator, Premiere Pro, etc.) and Document Cloud (Acrobat, Adobe Sign) suites.

The dominant model here is subscription-based, where users pay recurring fees for access to these applications.

Digital Experience (22.7%):

This segment focuses on providing solutions for marketing, advertising, and analytics.

Adobe Experience Cloud offers tools for businesses to manage customer experiences, digital marketing campaigns, and e-commerce.

Revenue is largely generated through subscriptions to these enterprise-level services.

Key aspects of Adobe's business model include:

Subscription-Based Model:

The transition to a subscription model has provided a stable and recurring revenue stream.

This model encourages continuous updates and improvements to their software.

Businesses with a recurring income stream are the best ones to own. This makes them less prone to the whims and whams of their customers.

Cloud-Based Services:

Adobe's cloud offerings allow for accessibility and collaboration, further enhancing the value of their products.

Focus on Digital Experiences:

Adobe's expansion into digital marketing and analytics reflects the growing importance of online presence for businesses.

In recent times, we have seen the emergence of smaller players, potentially threatening Adobe's market dominance.

Here’s an overview of the strong advantages that the company holds, along with the challenges that the company faces:

Strengths:

Dominance in Creative Software:

Adobe's Creative Cloud suite (Photoshop, Illustrator, Premiere Pro, etc.) remains the industry standard for many professionals. This gives them a significant market share and brand recognition.

Their long-standing presence has allowed them to build a robust ecosystem, with a seamless integration of their applications.

Successful Subscription Model:

The transition to a subscription-based model has provided a stable and recurring revenue stream, allowing for continuous development and innovation.

Imagine an individual who receives dividends every month into his/ her bank account. This person would be unstoppable. Same applies to a company.

Expansion into Digital Experience:

Adobe's Experience Cloud provides powerful tools for businesses, positioning them as a key player in the digital marketing and customer experience space.

AI Integration:

Adobe's focus on integrating AI, in particular with Adobe Firefly, gives them a strong position in the growing field of generative AI within creative fields.

Challenges:

Increased Competition:

Competitors like Canva and Affinity are offering cheaper alternatives.

Figma's rise in UI/UX design poses a challenge to Adobe.

The digital marketing area is very competitive with companies like Salesforce, and Oracle.

AI Monetization Uncertainty:

There is uncertainty surrounding how effectively Adobe can monetize its AI advancements.

Maintaining Innovation:

Adobe must continue to innovate and adapt to changing user needs and emerging technologies to maintain its competitive edge.

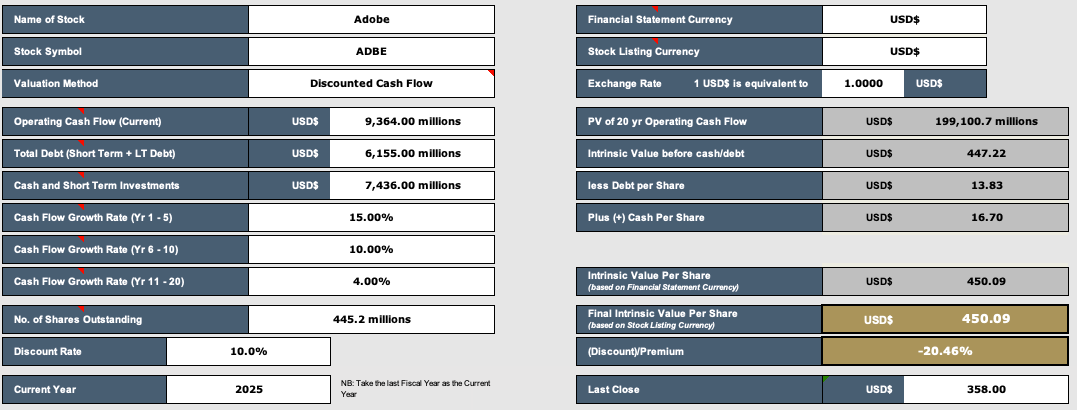

Valuation

The company is worth $450 in my calculations.

For me, I like to combine both fundamental and technical analysis (by identifying various buy levels).

My buy levels are set at prices at least 15% to 20% below the company’s fair value.

Unfortunately, with limited capital, it’s hard to initiate a position while there are so many other bargains in the market.

Summary

Adobe remains the market leader in the professional creative software industry, despite facing increasing competition from more affordable and user-friendly alternatives.

Humans are creatures of habit.

If you’re a creative professional who spent years learning to use Adobe’s creative software, it would be a tough to start from scratch and learn a new software.

Ultimately, the company’s success hinges on their ability to effectively monetize AI, continue to innovate, and adapt to the evolving market.